Raumbeispiel

416

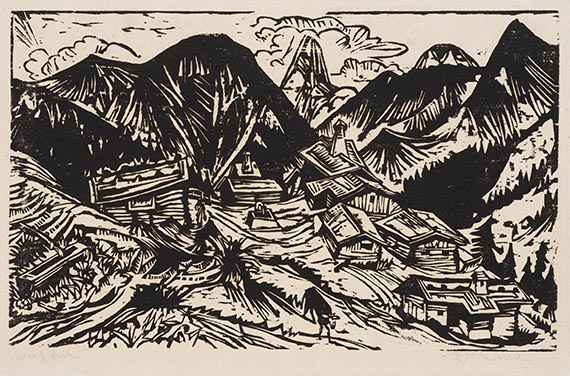

Ernst Ludwig Kirchner

Stafelalp mit Tinzenhorn, 1917.

xilografia

Stima: € 25,000 / $ 26,750

Stafelalp mit Tinzenhorn. 1917.

Woodcut.

Signed and inscribed "Handdruck". From an edition of only 21 known copies. On laminated blotting paper. 34.5 x 55.5 cm (13.5 x 21.8 in). Sheet: 39,3 x 58,4 cm (15,4 x 22,9 in).

The work is registered in Hermann Gerlinger Collection under the number SHG 775a. [CH].

• Hand-printed by the artist.

• During Kirchner's very first stay on the Stafelalp (above Davos) in 1917, he created 13 woodcuts, which are among the highlights of his oeuvre.

• Woodcuts play a particularly important role in Ernst Ludwig Kirchner's rich graphic oeuvre.

• Extremely detailed and very elaborate compositions.

• Only three copies of this woodcut have been offered on the international auction market in the last 20 years (source: artprice.com).

• Many of the 21 known copies of this woodcut are museum-owned, including the Museum of Fine Arts in Boston, the Philadelphia Museum of Art, the New York Public Library, the Albertina in Vienna, the Staatliche Museen zu Berlin, the Kunstmuseum Bern, the Stiftung Museum Kunstpalast, Düsseldorf, and the Kunstmuseum Winterthur.

PROVENANCE: Presumably Dr. Christian Adolf Isermeyer Collection, Berlin/Hamburg (with a hand-written ownershipnote on the reverse).

Hermann Gerlinger Collection, Würzburg (acquired in 2002, Galerie Kornfeld, Bern, with the collector's stamp, Lugt 6032).

EXHIBITION: Buchheim Museum, Bernried (permanent loan from the Hermann Gerlinger Collection, 2017-2022.

LITERATURE: Günther Gercken, Ernst Ludwig Kirchner. Kritisches Werkverzeichnis der Druckgraphik, vol. 4 (1917-1919), Bern 2015, no. 854 I (of II, illu.).

Annemarie and Wolf-Dieter Dube, E. L. Kirchner. Das graphische Werk, Munich 1967, no. H 301.

Gustav Schiefler, Die Graphik Ernst Ludwig Kirchners, vol. 2 (1917-1927), Berlin-Charlottenburg 1931, no. H 279.

- -

Galerie Kornfeld, Bern, 229th auction (Ist part), 175 ausgewählte Werke des 19. und 20. Jahrhunderts, June 21, 2002, lot 89 (full-page illu.).

Called up: June 8, 2024 - ca. 17.21 h +/- 20 min.

Woodcut.

Signed and inscribed "Handdruck". From an edition of only 21 known copies. On laminated blotting paper. 34.5 x 55.5 cm (13.5 x 21.8 in). Sheet: 39,3 x 58,4 cm (15,4 x 22,9 in).

The work is registered in Hermann Gerlinger Collection under the number SHG 775a. [CH].

• Hand-printed by the artist.

• During Kirchner's very first stay on the Stafelalp (above Davos) in 1917, he created 13 woodcuts, which are among the highlights of his oeuvre.

• Woodcuts play a particularly important role in Ernst Ludwig Kirchner's rich graphic oeuvre.

• Extremely detailed and very elaborate compositions.

• Only three copies of this woodcut have been offered on the international auction market in the last 20 years (source: artprice.com).

• Many of the 21 known copies of this woodcut are museum-owned, including the Museum of Fine Arts in Boston, the Philadelphia Museum of Art, the New York Public Library, the Albertina in Vienna, the Staatliche Museen zu Berlin, the Kunstmuseum Bern, the Stiftung Museum Kunstpalast, Düsseldorf, and the Kunstmuseum Winterthur.

PROVENANCE: Presumably Dr. Christian Adolf Isermeyer Collection, Berlin/Hamburg (with a hand-written ownershipnote on the reverse).

Hermann Gerlinger Collection, Würzburg (acquired in 2002, Galerie Kornfeld, Bern, with the collector's stamp, Lugt 6032).

EXHIBITION: Buchheim Museum, Bernried (permanent loan from the Hermann Gerlinger Collection, 2017-2022.

LITERATURE: Günther Gercken, Ernst Ludwig Kirchner. Kritisches Werkverzeichnis der Druckgraphik, vol. 4 (1917-1919), Bern 2015, no. 854 I (of II, illu.).

Annemarie and Wolf-Dieter Dube, E. L. Kirchner. Das graphische Werk, Munich 1967, no. H 301.

Gustav Schiefler, Die Graphik Ernst Ludwig Kirchners, vol. 2 (1917-1927), Berlin-Charlottenburg 1931, no. H 279.

- -

Galerie Kornfeld, Bern, 229th auction (Ist part), 175 ausgewählte Werke des 19. und 20. Jahrhunderts, June 21, 2002, lot 89 (full-page illu.).

Called up: June 8, 2024 - ca. 17.21 h +/- 20 min.

Kirchner arrived in Davos for the second time on May 8, 1917 to, as he wrote to his friend, the architect and designer Henry van de Velde, "complete my cure". During the summer, Kirchner lived with a nurse in the "Rüesch Hut" on the Stafelalp above Frauenkirch. Although he suffered from paralysis and was unable to write his own letters, he created landscapes and portraits of his new living environment that were characterized by an unbroken, elemental spirit of survival. And yet, Kirchner still had nightmarish fears and could not find peace. After a visit to the Stafelalp, Henry van de Velde persuaded Kirchner to confide in the psychiatrist and psychoanalyst Ludwig Binswanger. From mid-September 1917, Kirchner spent ten months at the Bellevue Sanatorium in Kreuzlingen on Lake Constance. Impressed by the nature that he saw right before his eyes, Kirchner depicted the steep alpine meadows with the "Alphütten", his view gliding across the gently rolling meadows interspersed with coarse rocks and weather-beaten wooden huts, sketching the narrow paths along the slope up to the nearby mountain plateau with more huts, giving contour to the forests and pastures. And Kirchner marked the mountain backdrop "Altein" on the other side of the valley with the omnipresent, striking Tinzenhorn, a mountain that towers over Kirchner's landscapes like a landmark. One can sense Kirchner's struggle to convey his fascination for the new mountain world in the woodcut, to 'reinvent' nature in detail. For Kirchner, the mountain dwellers he photographed became friends, whose habitat he commemorated in his early Davos landscapes. Kirchner also photographed the Stafelalp in the view from his summer hut and adopted the motifs for his view of the mountain village, as is the case with this large woodcut from 1917. Kirchner increasingly developed his Davos style and distanced himself from the original "metropolitan expressionism" of the Dresden and Berlin. [MvL]

416

Ernst Ludwig Kirchner

Stafelalp mit Tinzenhorn, 1917.

xilografia

Stima: € 25,000 / $ 26,750

Commissione, tassa e diritti di seguito

Quest'oggetto viene offerto con regime fiscale normale o con imposizione sul margine di profitto.

Calcolo commissione particolare sul margine del profitto:

- Prezzo d’aggiudicazione fino a 800.000 euro: provvigione del 32%.

- Per la parte del prezzo d’aggiudicazione superiore a 800.000 euro si calcola una provvigione del 27%, che viene aggiunta a quella relativa alla parte del prezzo d’aggiudicazione fino a 800.000 euro.

- Per la parte del prezzo d’aggiudicazione superiore a 4.000.000 euro si calcola una provvigione del 22%, che viene aggiunta a quella relativa alla parte del prezzo d’aggiudicazione fino a 4.000.000 euro.

Il prezzo d’acquisto comprende l’imposta sul valore aggiunto in vigore in quel momento, attualmente il 19%.

Calcolo regime fiscale normale:

Prezzo di aggiudicazione fino a 800.000 €: supplemento del 27%, più l´IVA legale

Prezzo di aggiudicazione superiore a 800.000 €: Parte del prezzo fino a 800.000 € supplemento del 27 %, parte del prezzo che supera i 800.000 € supplemento del 21%, a talvolta maggiorato dell'IVA legale.

Prezzo di aggiudicazione superiore a 4.000.000 €: Parte del prezzo che supera i 4.000.000 € supplemento del 15%, a talvolta maggiorato dell'IVA legale.

La preghiamo di avvisarci prima della fatturazione nel caso in cui desidera applicare il regime fiscale normale.

Calcolo diritti di seguito:

Per le opere originali di arti figurative e fotografie di artisti viventi o deceduti da meno di 70 anni soggette al diritto di seguito, in tutti i casi suddetti viene riscossa in aggiunta, a liquidazione della compensazione del diritto di seguito dovuto dalla casa d'aste ai sensi del § 26 della legge tedesca sul diritto d'autore (Urheberrechtsgesetz, UrhG), una compensazione del diritto di seguito con le percentuali indicate nel § 26 2° comma UrhG, che attualmente sono le seguenti:

4 per cento della parte del ricavo della vendita da 400,00 euro a 50.000 euro,

un altro 3 per cento della parte del ricavo della vendita da 50.000,01 a 200.000 Euro,

un altro 1 per cento della parte del ricavo della vendita da 200.000,01 a 350.000 Euro,

un altro 0,5 per cento della parte del ricavo della vendita da 350.000,01 a 500.000 euro e

un altro 0,25 per cento della parte del ricavo della vendita superiore a 500.000 euro.

L’importo complessivo della compensazione del diritto di seguito derivante da una rivendita è pari al massimo a 12.500 euro.

Calcolo commissione particolare sul margine del profitto:

- Prezzo d’aggiudicazione fino a 800.000 euro: provvigione del 32%.

- Per la parte del prezzo d’aggiudicazione superiore a 800.000 euro si calcola una provvigione del 27%, che viene aggiunta a quella relativa alla parte del prezzo d’aggiudicazione fino a 800.000 euro.

- Per la parte del prezzo d’aggiudicazione superiore a 4.000.000 euro si calcola una provvigione del 22%, che viene aggiunta a quella relativa alla parte del prezzo d’aggiudicazione fino a 4.000.000 euro.

Il prezzo d’acquisto comprende l’imposta sul valore aggiunto in vigore in quel momento, attualmente il 19%.

Calcolo regime fiscale normale:

Prezzo di aggiudicazione fino a 800.000 €: supplemento del 27%, più l´IVA legale

Prezzo di aggiudicazione superiore a 800.000 €: Parte del prezzo fino a 800.000 € supplemento del 27 %, parte del prezzo che supera i 800.000 € supplemento del 21%, a talvolta maggiorato dell'IVA legale.

Prezzo di aggiudicazione superiore a 4.000.000 €: Parte del prezzo che supera i 4.000.000 € supplemento del 15%, a talvolta maggiorato dell'IVA legale.

La preghiamo di avvisarci prima della fatturazione nel caso in cui desidera applicare il regime fiscale normale.

Calcolo diritti di seguito:

Per le opere originali di arti figurative e fotografie di artisti viventi o deceduti da meno di 70 anni soggette al diritto di seguito, in tutti i casi suddetti viene riscossa in aggiunta, a liquidazione della compensazione del diritto di seguito dovuto dalla casa d'aste ai sensi del § 26 della legge tedesca sul diritto d'autore (Urheberrechtsgesetz, UrhG), una compensazione del diritto di seguito con le percentuali indicate nel § 26 2° comma UrhG, che attualmente sono le seguenti:

4 per cento della parte del ricavo della vendita da 400,00 euro a 50.000 euro,

un altro 3 per cento della parte del ricavo della vendita da 50.000,01 a 200.000 Euro,

un altro 1 per cento della parte del ricavo della vendita da 200.000,01 a 350.000 Euro,

un altro 0,5 per cento della parte del ricavo della vendita da 350.000,01 a 500.000 euro e

un altro 0,25 per cento della parte del ricavo della vendita superiore a 500.000 euro.

L’importo complessivo della compensazione del diritto di seguito derivante da una rivendita è pari al massimo a 12.500 euro.